Retirement Routes: Cash

MORE ARTICLES

Last week we looked at flexible income (or drawdown), along with the advantages and things to consider when going down the flexible income route.

This week, we’re looking at cash.

In this blog:

- What does it mean to take your pension pot as cash?

- Advantages of cash,

- Considerations before choosing cash, and

- Support on your journey

What does it mean to take your pension pot as cash?

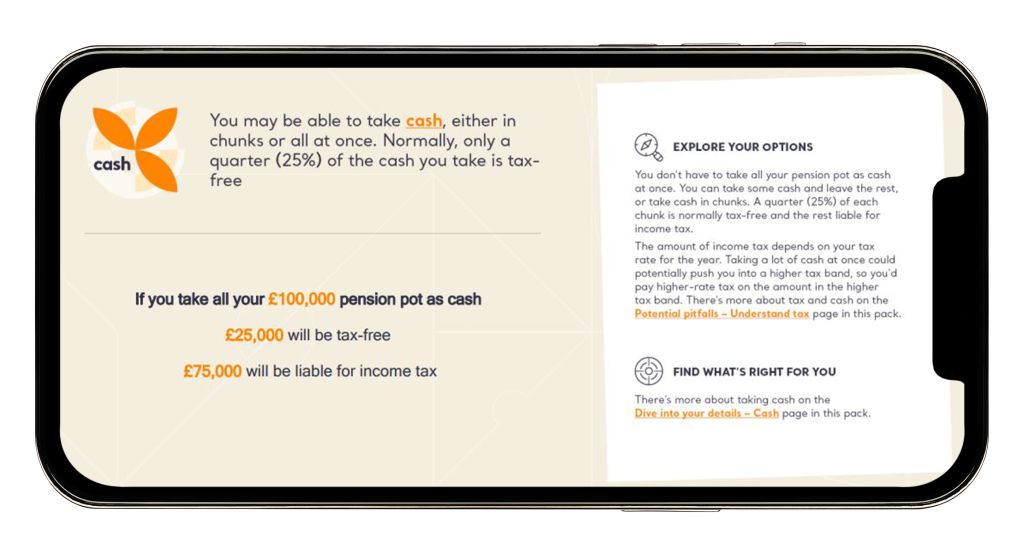

Depending on what your pension provider offers, you may be able to simply take cash out of your pension pot. You can either take one single cash amount or a number of smaller cash amounts over several months or years.

Each time you take money out, one-quarter is normally tax-free, and you pay income tax on the remaining three-quarters.

Advantages of cash

Flexibility and control

One of the biggest advantages of managing your retirement savings in this way is the sheer flexibility it offers. Imagine being able to access any amount of cash you need, whenever you need it, for whatever purpose you desire. The only snag? Be mindful of the Money Purchase Annual Allowance which restricts the amount of future pension savings you can make without incurring a tax charge. However, there is also the option of putting the cash into an Individual Savings Account (ISA) or a similar savings scheme.

Investment freedom

Taking cash out of your retirement savings can give you more freedom to invest it in a way that suits you – as you’re not tied to the investment options from pension providers. For example, as mentioned above, you could put the cash into an ISA or another non-retirement investment arrangement. If you’re still working and have access to your employer’s pension scheme, you should bear in mind that investing your money elsewhere could result in you losing out on employer contributions.

Can be tax efficient

One of the most compelling benefits of the potential for tax efficiency. Typically, 25% of any withdrawal you make is tax-free, which doesn’t impact your personal income tax allowance – the amount you can earn in a year before you start to pay income tax (the standard personal allowance is currently set at £12,570). You can manage the amount of tax you pay by being careful about how much you take out.

For example:

- Assume you withdraw £16,000.

- Out of this, £4,000 (one quarter) is tax-free. This leaves £12,000 that could be subject to tax.

- Assuming you’re entitled to the standard income tax personal allowance of £12,570, the whole £16,000 could be tax-free – as the £12,000 is below the personal income tax allowance.

You can use a tax calculator, like this one from MoneyHelper, to work out how much tax you might pay on your cash.

Top up gaps in your income

If you’ve got other pension savings and are careful to manage the tax, taking cash to top up gaps in your income can be a good use of a small pension pot.

Considerations before choosing cash

Be aware of unexpected tax

Taking a large lump sum from your pension pot could lead to an unwelcome surprise when it comes to paying tax. If the amount you withdraw, when combined with your other income for the year, bumps you into a higher tax bracket, you might find yourself paying more tax than expected. It’s important to understand how tax brackets work and the potential impact on your finances before making a withdrawal.

Future income

Dipping into your pension pot now could mean there’s less in it for the future – even if you’re planning to pay in more. Every pound you withdraw now is a pound that won’t grow over time through investment returns. Could this leave you with enough to live on? Consider the long-term implications when withdrawing cash from your pension pot. Planning ahead could mean you have a steady income stream later on.

Remember – investments can go down in value, and you may get back less than the contributions you pay in.

Investment and inheritance tax

The tax advantages of keeping your money in a pension are significant. Once you move your money somewhere else (aside from a tax-efficient ISA), you lose the benefits and may have to pay taxes on any investment gains.

Pensions also often offer inheritance tax benefits, as money within a pension doesn’t typically count towards your estate for inheritance tax purposes. However, if you withdraw cash, you might unknowingly increase your estate’s value and its potential inheritance tax liability.

State benefits and risks

If you get any income-related state benefits, such as Universal Credit, taking cash could affect the amount of benefits you get (as it counts towards your income). Also, if you have outstanding debts, creditors might be able to claim against the cash you withdraw.

Tax planning

If you’re considering drawing from your pension while continuing to contribute to a defined contribution (DC) scheme, it’s important to understand the impact on your tax relief. The Annual Allowance is a limit on the maximum pension contributions that can be paid each tax year before a tax charge applies. This is usually £60,000 (2024/25) and includes both yours and your employers’ contributions.

However, initiating withdrawals from your retirement benefits while still contributing to your pension can reduce this allowance to just £10,000 – known as the Money Purchase Annual Allowance (MPAA). This could limit the tax advantages of future retirement savings, highlighting how important financial planning is when thinking about ongoing pension contributions and withdrawals.

Support on your journey

While cash offers flexibility and control over your retirement income, it comes with its own set of responsibilities and risks. It’s important to approach these challenges with caution and, where possible, seek professional advice to help navigate the journey.

Guidance

Pension Potential, a service from Punter Southall, can help you explore how taking cash could work for you. Just fill in the short form on the Pension Potential hub to download a free, personalised pack and explore how you could take your retirement benefits as cash.

Alternatively, you can get guidance about the different ways to take DC retirement savings through Pension Wise. If you’re aged 50 or over, you can book a free guidance call.

Advice

Taking cash can be complicated. Because of this, you might want regulated financial advice. A good financial adviser will aim to get to know you and your circumstances. This will enable them to understand what’s important to you and what you’re trying to achieve with your retirement savings, so they can work with you to help you achieve your retirement vision in an effective and economical way.

Individual financial advice is available through Foster Denovo, the parent company of Secondsight and Aspire to Retire.

>You can contact the team by calling 0330 332 7866, or by emailing advise-me@fosterdenovo.com. Foster Denovo will explain any fees clearly in advance.

You can also find more information on getting guidance and advice on our ‘Help and support’ page.

Join us next week as we look at another retirement route: mixing your options.

Related Blog Articles

We think you may also be intertested in these: