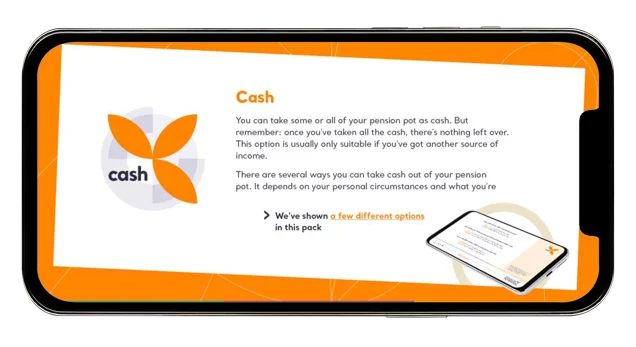

Retirement Routes 3: Cash

MORE ARTICLES

Taking the cash exit

Taking cash, at first sight, looks easy. As a general rule you simply take it out if your pension pot – either in chunks or all at once.

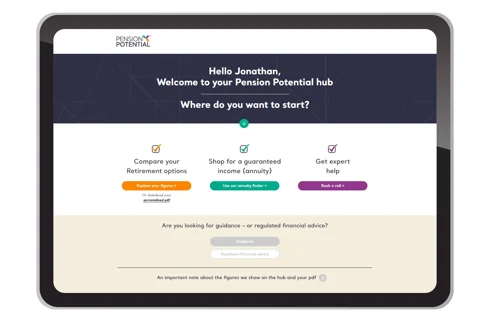

Pension Potential is a free-to-use, no obligation online hub which gives you the power to maximise your Pension Potential. It can help you understand if cash is a good option for you. Go to the Pension Potential hub and download a free pack showing your personalised options for taking your retirement benefits.

1. Taking it all at once

You can take the whole of your pension savings as cash if you want to. Most people aren’t likely to do this unless they’ve got other sources of income. But it’s there as an option.

One-quarter of the cash you take is tax-free. This is on top of your personal income tax allowance – the amount you can earn in a tax year (6 April to 5 April) before you start to pay income tax. The standard allowance is currently £12,570 a year.

💡 Pension Potential can show you personalised examples of how much cash you could get from your pension savings, and how much of it would be potentially tax-free. Go to the Pension Potential hub and fill in the form to get personalised examples.

2. Taking a bit at a time

Or, you can take as much or as little cash as you like and use it in any way you want. The one thing you need to be careful of is putting it back into your pension, as there are rules to stop you ‘recycling’ tax-free cash back into a pension (and potentially getting tax relief on it).

If you take only part of your cash, remember the rest stays invested – so you‘ll need to make sure you’re happy with your investment choices.

💡 Pension Potential uses your personal information to show you examples of what you could get if you take cash in different ways – such as in three equal chunks, or 20% now.

3. Watching your tax

You can manage the amount of tax you pay by being careful about how much you take out.

For example, if you took £16,000, one-quarter of this – £4,000 – is tax-free. This leaves £12,000 that could be taxed. If you haven’t got any other income in the tax year, and are entitled to the standard £12,570 allowance, the whole £16,000 is tax-free as the £12,000 is below the allowance.

But – if three-quarters of the cash you take, added to your other income for the tax year, pushes you into a higher income tax bracket, you could pay more tax than you expected.

4. Clever timing

If you do want to take a large amount of cash that could push you into a higher tax bracket, you could be clever with the timing. Spread taking your cash across the end of one tax year and the beginning of the next and you’ll be taking a lower amount in each tax year – which could help you avoid the higher rate of tax.

What Pension Potential can do for you

Pension Potential can help you explore how taking cash could work for you.

Fill in the short form on the Pension Potential hub to get your personalised quotes and examples. At any point in your Pension Potential journey, you can get expert help – so if you’re struggling to decide what to do or want help using the hub, just book a call with a retirement expert. They’re ready and waiting to help you reach your Pension Potential.

Related Blog Articles

We think you may also be intertested in these: