Visualise it, and make it happen

We’re all different, with different needs and expectations, and it’s important you know your options for making your pension fit for YOUR needs. Knowledge is power.

First though – take note!

We’re talking here about defined contribution or DC pensions, where you build up a pension pot based on contributions from you, contributions from your employer and growth on your investments. If you’re building up benefits in a workplace pension it’s most likely to be DC. Ask your employer or pension provider if you’re not sure.

1 | Know why your workplace pension is a great way to save

There are reasons galore – but here are some of the best reasons.

- As a UK resident, you are entitled to tax relief on your pension contributions (within certain limits, see below) – so for every £40 you put into your pension, the government adds at least another £10. You could be entitled to more tax relief if you pay income tax at a higher rate than the basic rate of 20%.

- You get more money from your employer, as they contribute to your retirement savings.

- Your savings are invested to help them grow. Although there may be ups and downs, over the long term they’re expected to grow more than money in a bank or building society account.

- Saving regularly also helps you in a couple of ways. See ‘tips for boosting your workplace pension’ to find out more.

-

Your workplace pension may come with features like benefits for your dependants if you die while working for your employer.

-

You have a choice of options for your retirement income, including protection for your dependants.

2 | Save the right amount for YOU

How much do you need to save? Probably more than you think.

The minimum contribution (including contributions from an employer) to most UK workplace pensions is usually 8% of ‘pensionable salary’ (note there are different definitions of pensionable salary that an employer can use and this may affect the minimum contribution level). It’s unlikely, however, that the minimum contribution level will be enough to meet your financial needs in retirement.

If you’ve been through ‘Creating your retirement vision’ you’ll hopefully know whether or not you are likely to have a shortfall in retirement income and need to be saving more.

Could you benefit from saving more than the minimum?

If your employer offers matching contributions, does it make sense for you to save at the highest level your employer matches, as long as you can afford to.

Here are some tips for boosting your workplace pension

Increasing your regular contributions could be quite a painless way to put more into your retirement savings. Even a small regular increase can add up over time. Remember, saving regularly means you benefit from:

- compounding (you earn investment returns or interest on the returns or interest you’ve previously earned, so your savings grow over time and the rate they grow at gets faster – though growth can never be guaranteed and you could also get back less than you invested), and

- pound-cost averaging (where you buy more investment units when investment values fall, so you have more units to increase when investment values rise).

And don’t forget the tax relief!

If you’re near to taking your retirement benefits, it might make sense to increase your contributions as much as you can afford to maximise your pension pot. Depending on what your scheme offers you may be able to change your regular contribution rate online, or by filling in a contribution change form. Check with your employer or pension provider.

Check whether your employer offers matching contributions. This means the more you put into your retirement savings the more your employer will add, up to a limit. If you’re not saving at the highest level that gets matching contributions, you’re missing out on extra money from your employer.

Even if you’re saving at the highest level that gets matching contributions, this doesn’t stop you saving more if you can afford to. Depending on your scheme, these extra contributions may be called additional voluntary contributions (AVCs). Like standard contributions, AVCs benefit from tax relief (up to certain limits – see Know the limits) and will help to increase your retirement savings.

As well as – or instead of – increasing your regular contributions you can make one-off contributions. This could be useful, for example, if you get a bonus or someone leaves you money in their will. You may be able to do this online or you may have to fill in a form, depending on what your pension provider offers. One-off contributions benefit from tax relief (up to certain limits – see Know the limits) but, depending on your scheme, you may have to reclaim the tax yourself by filling in a self-assessment tax return. Your employer or pension provider will be able to tell you whether you’ll have to do this

You could think about increasing your regular contributions every time you get a pay rise? You’ll hardly notice it, but it still means more going into your retirement savings.

3 | Know the limits

To get the best value from your pension contributions and avoid paying too much tax, you need to know your pension tax allowances.

If you go over any of the allowances, you’ll have to pay a tax charge on the amount over the allowance.

To note please: Figures used are based on legislation for the 2025/26 tax year which may change in the future.

An overview of the limits

You can put up to 100% of your earnings (net) into your retirement savings and still benefit from tax relief, as long as the total amount you and your employer contribute in a tax year is within the annual allowance.

The annual allowance is currently £60,000 for most people. It applies to all the pensions you’re actively saving into – so if you’re saving into a personal or stakeholder pension as well as your workplace pension, this counts towards the annual allowance.

Find out more about the annual allowance here.

Higher earners may have a lower – or ‘tapered’ – annual allowance.

Find out more about the tapered annual allowance here.

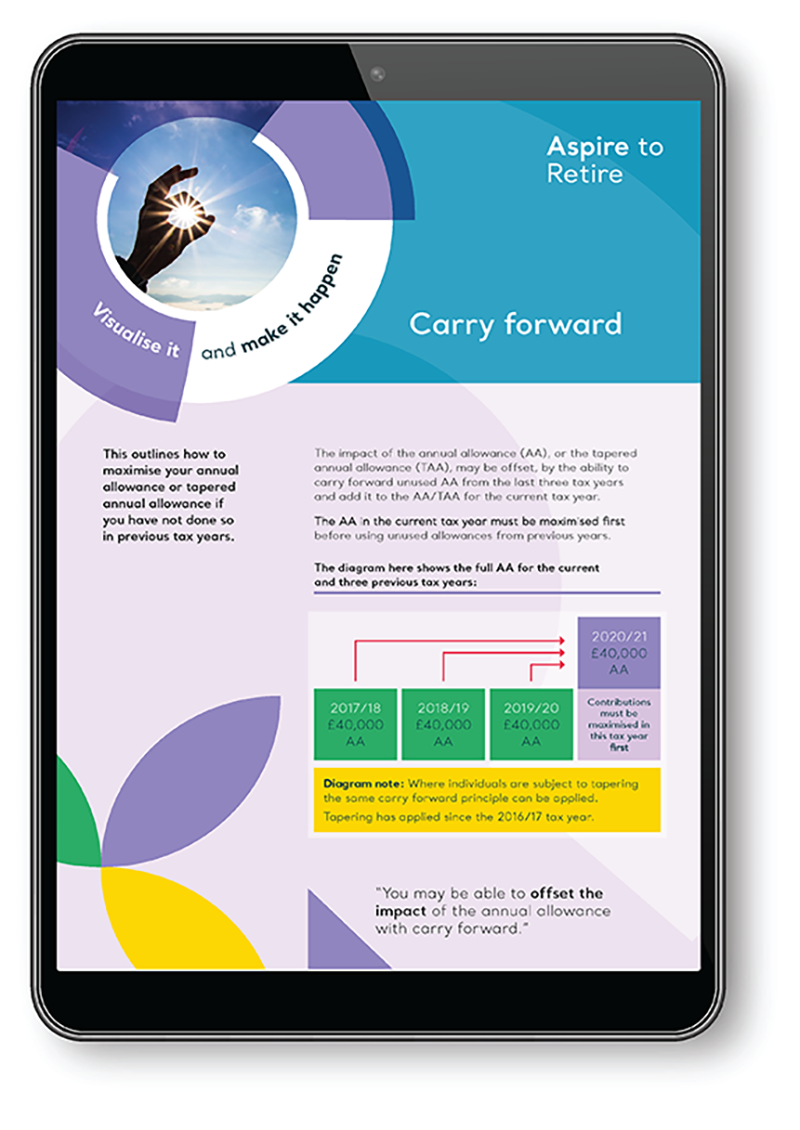

If you haven’t used up all your annual allowance in a tax year, you can carry it forward – enabling you to save more in the following tax year. You can carry forward up to three years’ unused annual allowance in this way.

Find out more about carrying forward your annual allowance here.

This allowance can apply if you take benefits in certain ways from your retirement savings while you are still saving. It reduces the amount that can be paid into your pension savings in a tax year without a tax charge applying. The money purchase annual allowance is £10,000 (for the 2024/25 tax year) and contributions from your employer also count towards this. It’s meant to discourage people from taking cash out of their retirement savings then putting it back in with tax relief. You can’t carry forward any of your Money Purchase Annual Allowance.

You can find out more about the money purchase annual allowance here.

With effect from 6 April 2024, the lump sum allowance limits the amount of tax-free cash you can withdraw from all your pensions throughout your lifetime to 25% of the value of the pot, up to a maximum of £268,275.

Anyone with a right to a higher tax-free cash entitlement will keep their right to take the higher amount

Find out more about the lump sum allowance here.

4 | Consider consolidation

If you’ve got several pension pots in different places, you might want to bring them all together before you retire.

Benefits of doing this could include:

- being able to see exactly how much you’ve got in your retirement savings

- dealing with only one provider

- easier access to your retirement income, as the money’s all in one place

- modern pension plans often have a wider range of investment options and lower investment charges compared to older pension plans.

You’ll need to choose a place to put all your pension pots.

- You might be able to add them to your workplace pension. You’ll need to ask your scheme administrator if you can transfer other pensions in, and what the rules are.

- You could choose to put all your pots together in a personal or stakeholder pension.

- Stakeholder pensions have a cap on their charges and a default investment option (which you automatically go into if you don’t make another choice). However this cap is higher than the maximum charge a workplace scheme can make in its default fund(s).

- Types of personal pension include self-invested personal pensions (known as SIPPs) which offer a wide range of investment options but may have higher charges.

As with everything, there are good and bad points you’ll need to weigh up carefully before making a decision. Consider your options carefully before consolidating, and if in doubt, speak to a financial adviser.

5 | Are your investment risks and rewards in line with your retirement goals?

While you were a long way from retiring, you probably wanted your investments to grow as much as possible.

The kind of investments that are likely to give the highest rewards over the long term also have the highest risk of falling in value in the short term. This is less of a problem when you’re further away from retiring and have enough time for long-term growth to make up for short-term falls in value.

As you get closer to taking your benefits, you may be more interested in protecting the value of the money you’ve built up. After all, you don’t want the value of your pension pot to plummet when you’re about to start taking benefits from it.

This is why most pension providers’ default investment options – which you’ll be in if you didn’t make another choice – move your savings into lower-risk investments as you get closer to your target retirement age. Lower-risk investments may give lower rewards, but they are also less likely to suffer sudden falls in value, which tends to be more valuable at this point.

If you’re not in the default investment option (or another ‘lifestyle strategy’ or ‘retirement pathway’ option that switches your investments automatically) you’ll need to decide whether to make the switch to lower-risk investments yourself.

NEXT UP:

Protecting your loved ones ![]()